EST. 2014

Monetization

Platform

WMG International (known as adWMG) provides pioneering ad tech solutions for advertisers and niche publishers worldwide. Tailored, tech-driven advertising to ace personalized goals.

Certified by:

For Direct

Publishers & SSPs

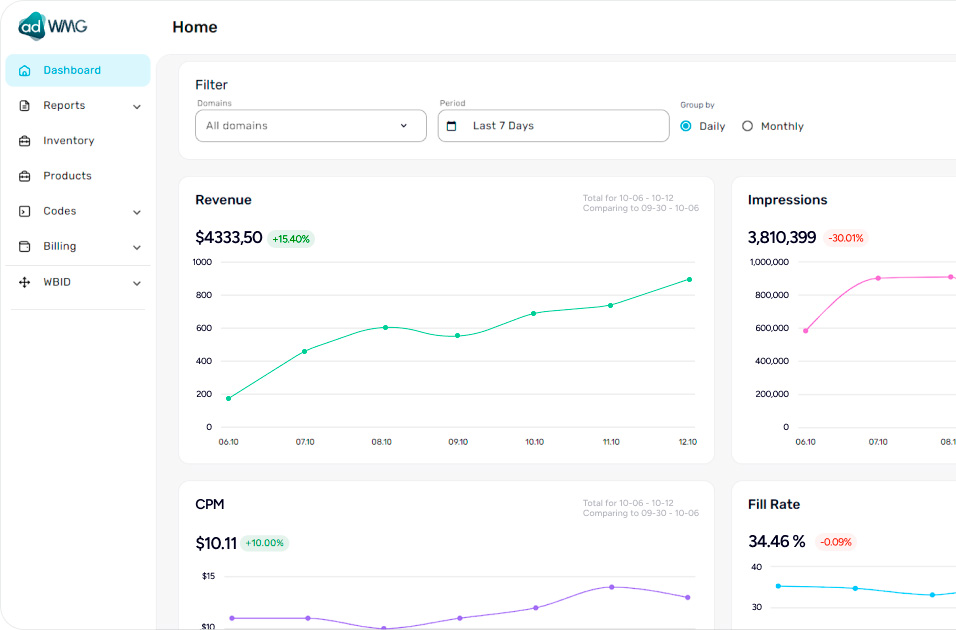

Our sophisticated Analytic Report feature can gather, generate, and analyze large amounts of data in real time. Protecting your information on our secure servers, WMG allows you to use numerous filters and metrics that allow you to build and customize effective monetization strategies.

They trust us:

JavaScript

Tag

Tag

openRTB

endpoint

endpoint

VAST

Prebid

Client Side

Client Side

1 Trillion

Ad requests monthly

100

High-quality SSPs

9 000

Direct Websites

10 000

Mobile applications

Simplifying complicated technologies, WMG

creates products for

programmatic monetization

creates products for

programmatic monetization

About us in the Media

adWMG & Azerion Enhanced Games Revenue Applying Cross-Device Targeting

adWMG is a part of global WMG International - a focused monetisation

and promotion platform focusing on

providing professional advertising

services for console game developers/

publishers and monetising web, CTV...

and promotion platform focusing on

providing professional advertising

services for console game developers/

publishers and monetising web, CTV...

How adWMG connects Xbox/Playstation inventory and mobile app installs

adWMG has developed a unique solution that maximises mobile app game conversion rates by effectively reaching mobile gaming audiences on console gaming devices (such as Xbox and PlayStation). This innovative approach...

How to drive user growth for console and PC games

In an increasingly competitive gaming landscape, getting your console or Steam title in front of the right players can be a major challenge. That’s where adWMG steps in – offering a flexible, no-risk model for performance-driven user...

WMG International ecosystem

Formats

Product

Device

Formats

Product

Integration

header bidding

header biddingwrapper

adWMG HB

adWMG HBadapter

header bidding

header biddinganalytics

wPlayer video

wPlayer videosolution

Mobile devices

Mobile devices Desktop

Desktop CTV

CTV

Technical core

Banner

Banner

Audio

Audio

DSP

Direct campaigns

BidSwitch

Header bidding

Authorized Buyer

SSP

Using the most contemporary technological stack, WMG International creates effective technical solutions for publishers worldwide

Jay Handline

Emin Alpan

Arthur Daniyarov

Shivamshree Urmaliya

Jay Handline

Sheby Ahamed

Hari